FEATURED NEWS - * COVER STORY *

Why Buyers are Caught in a Feeding Frenzy for Homes and How to Buy a House in this Tough Market

Written By Ryan Lessard (news@hippopress.com)

Images: Courtesy Photos

When Eva Stenberg of Newport started looking for a house last fall for her two college-age sons and a couple roommates to stay in while they attended school, she had no idea what she was getting herself into. She quickly had to raise her initial price range of $150,000 to $160,000 because all she could find in that range were mobile homes. She passed on a $200,000 home in Epsom because the location wasn’t ideal but has regretted it ever since — as she would soon learn, the competition for starter homes has reached a fever pitch over the past year.

“It was no longer people underbidding the requested price, it was people overbidding,” Stenberg said. “The pricing started to creep up on us, so it got harder and harder. And by the time we were in the January, February time frame, the houses were turning in three to five days. We didn’t even know it was on the market and it would already be pending.”

Each home she encountered was the target of a bidding war. Ultimately, she visited nearly 25 homes before closing on a house in Nottingham for $200,000. On average, Stenberg estimated, they looked at about three to five houses every weekend.

“I’d say a lot of them were bought before I could even get an appointment to look at them,” Stenberg said. “There were some that we went to go see and we found out that evening they were pending. We didn’t even have a chance.” What Stenberg encountered is happening across southern New Hampshire, and experts say it’s caused by record low housing supply and growing buyer demand.

Taking Stock

The state has fewer available houses on the market than ever before. According to the most recent data released by the New Hampshire Association of Realtors, there were 5,275 houses for sale statewide in April. That’s down from 7,726 in

April 2016 and 8,525 in 2015. And it’s the lowest it’s been since they started to track those numbers in 2005.

“We don’t physically have enough inventory for buyers who want to buy homes,” said NHAR President Rachel Eames.

While demand has gone up in the past year, Bill Ray at the New Hampshire Housing Finance Authority says inventory has not kept up, which makes the supply side the anomaly in this situation.

And the problem is not unique to houses. Apartment units are also extremely scarce. Ray said the 2017 rental housing report due later this month will show a continued decrease in the rental vacancy rate. Preliminary numbers show the vacancy rate for two-bedroom apartments (not counting subsidized units) to be at 1.4 percent, an all-time low.

“Since I have been here, in 21 years, I have not seen that,” Ray said. That dynamic is naturally raising rents, which in turn drives more people to seek homes. Robert Tourigny, the executive director of NeighborWorks Southern NH, said the tight housing market combined with the tight rental market has created a perfect storm for prices to skyrocket.

“I don’t recall seeing both of them as tight as they are right now. Usually if the home buyer market is really robust then it leaves some vacancies and such in the rental market. And the opposite is true,” Tourigny said. “But right now, what seems like the last few months, the demand on both sides, I think, is unprecedented.”

The main reason housing inventory is unusually low is that there aren’t enough new houses being built. Construction virtually stopped during the recession. This was partly due to a mass exodus of contractors during the recession. But for those developers who are still working in this industry, there are many barriers to new building new houses, from local ordinances to land availability and land prices.

“Access to financing for the buyers is always a challenge, as well as getting through the development approval process at the local level and zoning requirements,” Tourigny said.

And as long as the focus is on building multi-family rental units, Ray concludes that those projects must be more profitable. Right now, Ray said, the highest demand is among houses priced at $300,000 and below, which the Housing Authority defines as first-time homes. But those are not a priority for developers.

“We’re not seeing a lot of housing built for sale for under $300,000. In fact, I’m not sure if there’s any,” Ray said. Eames said developers are only building an estimated 20 percent of the housing stock that’s needed.

The market is tightest in the southern counties with the greatest populations: Hillsborough, Rockingham, Strafford and Merrimack. And as the state runs out of houses, more and more people are looking to buy houses.

Buying Power

The immediate driver of housing demand in the state is the economic recovery.

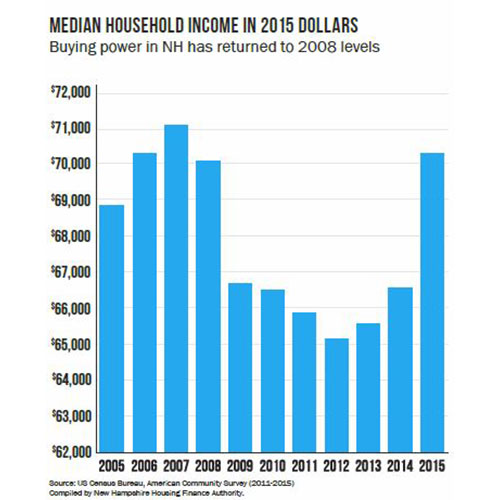

“What we’ve seen is economic improvement, especially in the southern part of the state,” Ray said. As a result, more people can afford homes than during the recession. According to a March report by the Housing Authority, median household income in 2015 roughly returned to 2008 levels, when inflation is accounted for.

The economic recovery also means an uptick in population. Ray said more people are migrating from Massachusetts and looking for homes. The state’s population is expected to increase by 100,000 over the next 25 years, according to Eames.

Young vs. Old

There is also increased competition over starter homes in the $200,000-to-$300,000 price range from different age groups.

Along with young, first-time homebuyers in their 20s and 30s, the market is also seeing a lot of middle-aged empty-nesters and Baby Boomers who are looking to downsize from a bigger, high-maintenance home to something more manageable. Ray said the older buyers often have a competitive edge.

“The downsizers bring equity and as a result they have cash to pay for the houses … and compete better than a first-time homebuyer,” Ray said.

Lisa Capicchioni, a senior loan officer at Residential Mortgage Services, has 25 years of experience in the local housing market. As a lender, she’s seen more buyers in their 40s and 50s who were able to sell their houses at a premium and come to buy smaller houses with more capital for down payments and closing costs.

And Capicchioni said they don’t even need to put down as much as 20 percent to gain an edge. Even with 5 or 10 percent down, they’re making more appealing offers than the zero-down governmentfinanced loans offered to some first-time homebuyers who can’t afford to make big down payments.

The disparity grows more pronounced when a house is in a bidding war.

“When you’re talking about first-time homebuyers, they’re more shackled because they don’t have the ability to keep going up on price,” Capicchioni said. Still, Ray said, the types of homes first time homebuyers and downsizers are looking for don’t always overlap. Downsizers, he said, are often looking for a smaller footprint, but they still want some of the nicer amenities, like granite countertops.

Prices Launching

Low supply and high demand mean higher prices, as any Economics 101 class would tell us. But the problem appears to be exacerbated on the demand side by demographic competition and on the supply side by burdensome regulations at the local level and fewer contractors. On top of that, an aging population getting reverse mortgages to stay in their homes longer and a younger population that moved back in with parents and grandparents have kept more houses from going on the market.

The last time the market was this hot was during the housing bubble, which saw median prices for single-family homes peak in New Hampshire at about $270,000 in 2005, according to data from the NH Realtors Association. In 2016, prices rose to about $249,000, just shy of 2004 prices. By April, median prices rose to $260,000.

Of course, the prices in the early 2000s were inflated by risky lending practices that drove up demand. Right now, Eames said, it’s a “slight” seller’s market because they stand to get asking price in most cases.

“It’s not like prices have gone totally crazy,” Eames said.

In this case, prices represent real value. As long as people can afford the higher prices, this situation will give sellers the advantage. According to data from the April realtors report, sellers were getting 98.1 percent of their listed price. That’s as high as it’s been since 2005.

“They’re getting top price, sometimes even over the listed price,” Capicchioni said.

How to Nab a House

When it comes to buying a house in this market, especially a first home, people need to be equipped with a combination of the common fundamentals and a few additional skills. For a lot of people, the struggle is caused by the speed with which they need to act. Among other things, it means people aren’t given enough time to mull over the major decision of buying a house.

“The market isn’t really allowing them to sit and absorb the numbers. They have to act quickly,” Capicchioni said. And that can mean missed opportunities. Melissa Starkey, the owner of Starkey Realty, said it’s important to be ready to pounce when the right house comes along.

“Be mentally prepared to offer right away if you like the house. Don’t make snap decisions that you’re going to regret. But … if you hem and haw it’s not going to be around,” Starkey said. That can make the process more stressful.

“I think it adds added stress and pressure for sure,” Eames said.

“You’re under the gun to get your offer in and hope it’s the best offer. People get very anxious.” Whether the buyers have had experience in the housing market before or not, they often have to adapt to the highly competitive environment.

Be Flexible

Ryan Tufts, a homeownership counselor at NeighborWorks, said there’s a house out there for everyone, even in this tight market. The trick is being open to change and compromise.

“The people who are most successful right now are the most flexible. Maybe it’s not the right part of town they wanted initially or maybe they made some compromise on how great of shape the home was in,” Tufts said.

He said virtually all of the people he’s helped counsel through the homebuying process have found a home by being flexible.

“If you’re going to come in saying I need a three-bedroom, two-bath on a nice quiet street with a two-car garage, this is my price range, in this part of town — OK, we’d all love that, but you might have to give up some piece of that,” Tufts said. Eva Stenberg, who bought a house in Nottingham for her two sons, said the trial and error and rapid-fire pace of her search helped to home in on which things she was willing to sacrifice.

“You have no ability to make a choice,” Stenberg said. “You had to learn what you were willing to accept and what you weren’t willing to accept so that you could jump on it.” It also took constant vigilance and keeping an open line of communication with her real estate agent, Starkey, and her lender.

Christine Paige and her husband Richard needed to downgrade from the 2,900-square-foot house they were renting in Epsom. She is 68 and Richard suffered a stroke, so shoveling their long, winding driveway in the winters became impossible. Paige wanted to get a house near the Seacoast, but she soon found that prices were too high and the houses were not always in good shape.

“There were just no homes out there anymore. No good homes,” Paige said.

She also didn’t expect the kind of competition they were up against, so, with the help of her realtor, Rachel Eames, and her loan officer, Carol Jordan at Merrimack Mortgage, she figured out a compromise: look at Seacoast area homes farther inland. She settled on a 2,025-square-foot house in Rochester. Paige says she’s a Type A personality and was stressed whenever she hit a bump in the road, like when the Rochester home had elevated levels of arsenic in the groundwater.

But she credits Eames and Jordan for jumping in at every step to make the process as painless as possible. The arsenic problem, for example, was resolved by getting an arsenic mitigation system installed. Capicchioni said it often takes first-timers losing out on two or three homes before they begin to reevaluate their approach.

Education

Tufts said one of the best ways to be prepared going into the homebuying process is to get educated on the process. This is especially helpful for first-timers but can also serve as a refresher course for someone who has bought a house before.

“For anyone who’s buying a house or interested in learning more about it, the main thing we offer is a workshop that’s geared toward teaching you the fundamentals of home-buying,” Tufts said.

In his workshop, Tufts goes over the benefits and downsides of owning a home and figuring out if it’s the right time to buy. The class goes over basic household budgeting, looking at savings, debts and credit scores. "Knowing what you can afford is important, Tufts said, because too often people bite off more than they can chew.

“The big thing we’ve encouraged throughout whatever the market is like is to really know that you can afford this payment that you’re stepping into and the additional costs of owning a house,” Tufts said. “Maybe their rent and actual mortgage payment might be a little bit equal but usually people are getting a bigger space, they’re going to have a higher utility [cost] so their actual costs are going to go up usually by hundreds of dollars a month in most cases.”

Then he brings in a lender to talk about mortgage options and assistance programs, followed by a real estate agent who talks about why it’s important to have an agent, the home search process and what a purchase-and-sale agreement looks like.

Finally, Tufts invites an insurance agent, home inspector and someone from a title company to go over the final steps, from making sure the house has good bones to considering different insurance options.

“I don’t expect anyone to leave this class a seasoned vet, but I want them to at least have some exposure to what they’re going to encounter so they can continue their research in an intelligent way,” Tufts said.

Build Your Team

As buyers like Stenberg and Paige can attest, having a good team behind you can be the difference between failure and success.

“Having a strong team is definitely something we would recommend,” Tufts said.

Tufts said it’s important to build a good relationship with your real estate agent, lender and possibly a homeownership counselor so that they can communicate with you and sellers and iron out all the difficult parts of the process. Buyers can often lose sight of their own control of the situation, so Tufts said buyers must keep asking questions and make sure their team knows what it is they want.

“Don’t forget that you’re the boss in this situation. No one is really getting paid until you buy the house,” Tufts said.

Real estate agents and lenders are all very skilled at what they do, Tufts said, so buyers need to pick people they are comfortable with on a social level.

“Find someone who talks more your speed and your language to work with you, and who’s available when you’re available,” Tufts said.

Availability is key, which is why Tufts recommends sticking with lenders who are local. Local lenders are more likely to pick up the phone when you need them. In a market where time is of the essence, it’s more important than ever to avoid situations where you’re waiting for days for a call back.

Prequalify

When asked what advice she would give to other homebuyers, Stenberg’s very first point is to start the loan process.

“Make sure you get prequalified. Find the range. Know your max limit,” Stenberg said.

Coming into the home search process with that knowledge will help to narrow your search and inform you when to back away from a bidding war when it starts to exceed your limit.

Robert Tourigny at Neighborworks said that while home prices are currently climbing, loan rates are still very good, hovering around 4 percent. “Fortunately, interest rates have remained quite low for an extended period of time,” Tourigny said.

But Stenberg cautions buyers to not get carried away by the bidding process.

As with many other recent homebuyers, she had to overbid to win her home by a few thousand dollars. But, in the end, she stayed within her price range and was able to do that because she kept in constant contact with her lender and kept sight of what her range was.

Town Research

Eames said that one way to stay limber and quick in the search and bidding process is to complete all the necessary research on the town and neighborhood in advance.

“Typically, for commuting purposes, buyers will be looking at three towns,” Eames said.

If you know what towns you’re looking in, all the research comparing crime statistics, municipal services and school districts can be done already. That way, you’re not scrambling to do extra homework when considering a home in what is likely to be a short window of opportunity.

Wants vs. Needs

One of the very first things Eames does when she sits down with a new client is discuss what a buyer wants and needs. Those things vary from person to person but the more an individual can categorize the things they’re looking for into those two columns, the more flexible they will be when it comes time to compromise and make a decision.

Eames defines wants as luxury items, amenities like a garden plot or a nice view. Needs, on the other hand will make or break a deal. So, if a buyer conflates wants with needs, they likely won’t find that perfect home in their price range.

Write a Letter

In addition to working with an agent to craft the best possible bid and act swiftly in the face of heightened time constraints, a personal letter to the sellers might provide that little extra icing on the cake. Lisa Capicchioni said a personal letter is an opportunity to talk about your story, the things you want for you and your family and maybe your personal struggles.

“So [sellers] can look at them as real people,” Capicchioni said.

The personal stories may tug at the heartstrings of the seller and help you stand out in a crowded field.

Sell First

If you’re coming into the market already a homeowner and you’re looking to buy a different home, often your bid will come with what’s called a home sale contingency. That’s a way to make sure you can transition seamlessly from one house to the next but it also represents a burden for a seller who may be eager to sell fast.

Melissa Starkey said home sale contingencies are a major obstacle to getting a bid accepted in this highly competitive market. A solution may be to sell your existing home first and figure out a temporary living situation while you look for the next home.

“One of the questions I ask sellers is, ‘Do you have a place to go?’” Starkey said.

Even the highest bid can be overlooked if there’s a contingency attached to it. That’s what happened with the home Christine Paige bought in Rochester. She said their bid was the second highest of five with about $10,000 over the asking price. The reason she got the house was that the highest bidder had a sale contingency.

Creative Capital

For young first-time buyers who are hoping to get a house with no money down, that may be possible in many cases still, but in particularly competitive regions it may be necessary to sweeten the deal with a small down payment. Of course, many people don’t have the kind of liquid capital that requires. So, Capicchioni said, it may require turning to family members for personal loans or cash gifts to raise the money needed.

If that’s still not possible, there are assistance programs that can help. The federal USDA rural development loan program provides 100 percent of the home price in certain designated rural areas, according to Tufts. It’s only available to first-time homebuyers. That leaves closing costs, but even then, that cost can be largely covered by the sellers in the negotiations.

In New Hampshire there’s also a tax credit program provided through the Housing Authority called the mortgage credit certificate that can provide up to $2,000 in tax credits per year. Tufts said you have to apply for that before you close on your loan and buyers qualify based on a household income level.